Emergency Fund Calculator

Calculate Your Emergency Fund

Where to Keep Your Fund

For maximum safety and growth, keep your emergency fund in a high-yield savings account (HYSA).

Recommended options (as of late 2025):

- Ally Bank: 4.20% APY, no fees, easy transfers

- Marcus by Goldman Sachs: 4.40% APY, no minimum balance

- Discover Bank: 4.10% APY, great app, instant transfers

- Capital One 360: 4.00% APY, integrates well with other accounts

Key features of a good emergency fund account:

- FDIC-insured up to $250,000

- High interest (4%+ APY)

- Easy access (24-48 hour transfers)

- Separate account with clear labeling

Your Emergency Fund Plan

Minimum Target

$0

3 months of expenses

Ideal Target

$0

6 months of expenses

Time to Reach Target

0 months

At your current savings rate

Recommended Action

Based on your inputs, you need to save $0 per month to reach your ideal emergency fund.

Most people think an emergency fund is just a pile of cash tucked away somewhere. But if you don’t know how much to save or where to put it, that pile might as well not exist. You could have $2,000 sitting in a checking account, only to watch it vanish the second your car breaks down or your paycheck gets delayed. That’s not an emergency fund - that’s a wish. Real emergency savings work when you need them most. They don’t sit idle. They don’t get mixed up with vacation money. They’re there - fast, safe, and ready.

How Much Do You Really Need?

The standard advice is three to six months of expenses. But that number means nothing if you don’t know what counts as an expense. It’s not your Netflix subscription or your monthly coffee habit. It’s the stuff that keeps your lights on and your food on the table.

Start with your fixed costs: rent or mortgage, property taxes, insurance (health, car, home), utilities, and minimum debt payments. Then add variable essentials: groceries, gas, medications, daycare, and basic transportation repairs. Don’t include dining out, shopping, or gym memberships. Those can wait.

Here’s how to calculate it: Add up all those monthly essentials. Multiply by three for a minimum buffer. Multiply by six if your income is unstable - if you’re freelance, commission-based, or work in a volatile industry. If you’re in a dual-income household with stable jobs, three months might be enough. If you’re the sole earner, aim for six. Some experts, like USAA, even suggest nine months if your job is unpredictable.

But here’s the truth: you don’t need to hit six months overnight. Start with $1,000. That’s the bare minimum to cover a sudden tire replacement, a broken appliance, or a small medical bill. Then build from there. NerdWallet says 44% of Americans can’t cover a $400 emergency without borrowing. If you’ve got $1,000, you’re already ahead of almost half the country.

What Counts as a Real Emergency?

Not every unexpected expense is an emergency. That’s where most people mess up. You bought a new phone because yours died? That’s not an emergency - that’s a replacement. Your kid needs braces? That’s a planned expense, even if it’s a surprise. An emergency has three traits: it’s unforeseen, essential, and urgent. If two out of three are true, you’re allowed to tap the fund.

Examples of real emergencies:

- Your car transmission dies and you rely on it to get to work

- You lose your job and have no income coming in

- A medical bill arrives you didn’t expect - say, an ER visit for your child

- Your roof leaks and water is damaging your floors

Examples that aren’t emergencies:

- Going on vacation because you need a break

- Upgrading to a newer iPhone

- Buying holiday gifts

- Fixing your lawn mower because you want it to look nicer

Ally Bank calls this the “two-out-of-three rule.” If you’re not sure, ask: Is this unavoidable? Is this necessary to keep life running? Is this happening right now? If yes to two, go ahead. If not, wait.

Where Should You Keep Your Emergency Fund?

Don’t keep it under your mattress. Don’t keep it in your checking account. And definitely don’t invest it in stocks or crypto. That’s not savings - that’s gambling with your safety net.

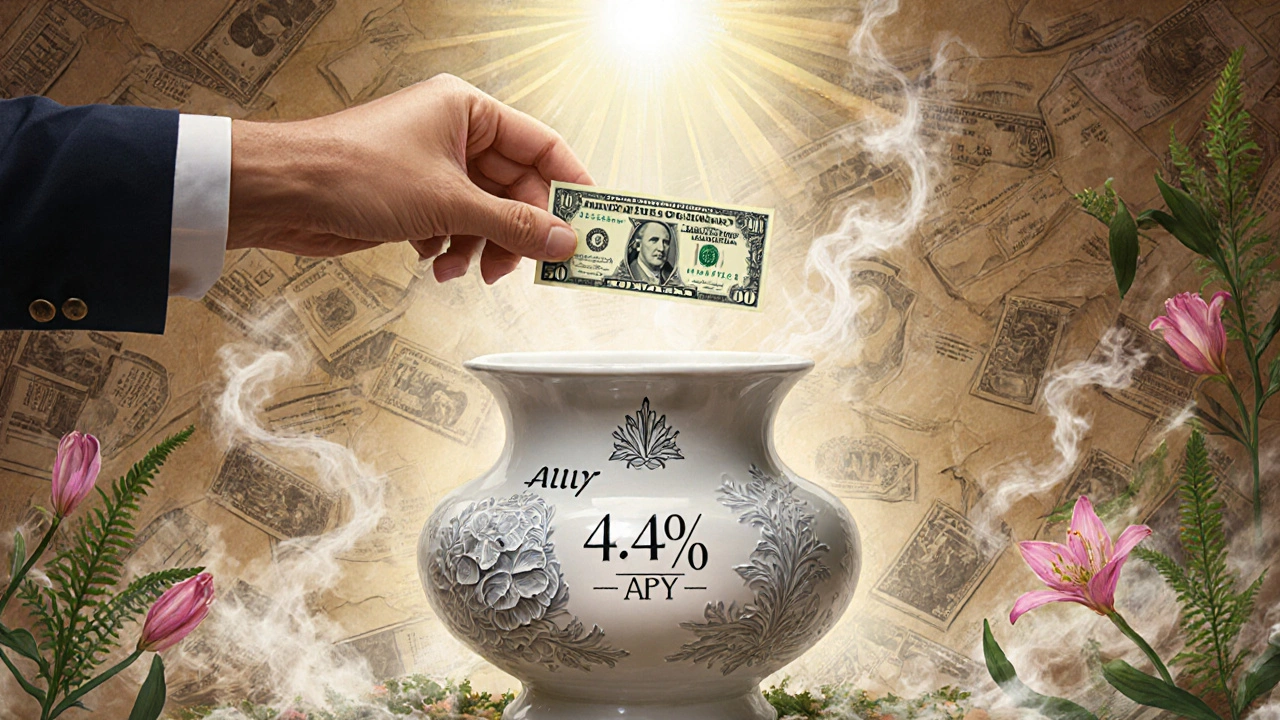

The only place that works is a high-yield savings account (HYSA). Why? Because it’s liquid, safe, and earns interest. You can access it within 24-48 hours. It’s FDIC-insured up to $250,000. And right now, you can earn between 4.1% and 4.4% APY - far better than the 0.01% you’d get from a regular bank.

Top options as of late 2025:

- Ally Bank: 4.20% APY, no fees, easy transfers

- Marcus by Goldman Sachs: 4.40% APY, no minimum balance

- Discover Bank: 4.10% APY, great app, instant transfers

- Capital One 360: 4.00% APY, integrates well with other accounts

Open one account. Label it clearly: “EMERGENCY FUND - DO NOT TOUCH.” Duke University found that people who labeled their accounts this way saved 27% more over time. It’s a mental barrier. And you need it.

Don’t link this account to your debit card. Don’t set up automatic payments from it. Make it slightly inconvenient to access. That’s the point. You want to think twice before spending it.

How to Actually Build It - Even If You’re Broke

You’re not going to save $10,000 in a month. But you can save $50 a week. That’s $200 a month. In 50 weeks, you’ve got $5,000. That’s a full three-month cushion for many people.

Here’s how to make it happen:

- Automate it. Set up a recurring transfer from your checking account to your emergency fund every payday. Even $25 per paycheck adds up. Most people who automate save 5-10% of their income without noticing.

- Use round-up apps. Apps like Digit or Qapital analyze your spending and move spare change - like the $3.47 left over from your coffee purchase - into savings. Users report 34% faster growth than manual saving.

- Start small, then scale. Got $500? Great. Now aim for $1,000. Then $2,500. Then your three-month target. NerdWallet says it’s okay to use the fund before you reach your goal. Replenish it. That’s not failure - that’s life.

- Combine with debt payoff. If you have credit card debt over 7% APR, pay the minimum while building your $1,000 fund. Then focus on the full emergency fund. SoFi recommends this hybrid approach. It stops the bleeding while you build your shield.

One person on Reddit saved $5,000 in 14 months by cutting one subscription, cooking at home three extra nights a week, and automating $125 from each paycheck. That’s not genius. That’s consistency.

What Happens When You Use It?

Some people feel guilty when they use their emergency fund. They think they’ve failed. But that’s the wrong mindset. The fund exists to be used. It’s not a trophy. It’s a tool.

When you use it - for a car repair, a medical bill, a job loss - you’re doing it right. The goal isn’t to never touch it. The goal is to never have to go into debt because of it.

After you use it, rebuild it. Treat it like a replenishable resource. Set a new goal: “I’ll put back $200 a month until I’m back to $5,000.” That’s not a setback. That’s the whole point of having it.

Studies show households with emergency savings are 32% less likely to experience financial distress during economic downturns. That’s not luck. That’s preparation.

Why Not Just Use a Credit Card?

Some economists argue that if you have great credit, you can just use a 0% APR credit card for emergencies. But that’s risky.

What if you lose your job? Then you can’t pay it off. What if the card issuer changes the terms? What if you forget to pay it off before the promo ends? Then you’re stuck with 24.75% interest - the average rate for credit cards in Q2 2023, according to the Federal Reserve.

An emergency fund is cash. No interest. No penalties. No fine print. You don’t need to qualify. You don’t need to wait for approval. You just use it.

And if you’re one of the 31% of households earning under $40,000 who don’t have an emergency fund? Credit cards won’t save you. They’ll bury you.

Real-World Failure Stories

One person kept their emergency fund in a high-yield investment account, thinking they’d earn more. When their child needed emergency surgery, the market had dropped 22%. They had to sell at a loss. That’s not an emergency fund - that’s a gamble.

Another person used their checking account for everything. When their car broke down, they spent $3,200 and had to overdraft. Then they paid $300 in fees. That’s two emergencies: the car, and the overdraft.

And then there’s the person who saved $1,500 - then spent it all on a wedding gift. No label. No boundaries. No plan. That’s not savings. That’s a habit.

Don’t be that person.

What’s Changing in 2025?

Emergency funds aren’t just a personal thing anymore. Employers are starting to offer them as part of benefits. Twenty-eight percent of large companies now help employees save through payroll deductions - some even match contributions. That’s new.

The Consumer Financial Protection Bureau’s Emergency Savings Project has pushed banks to create “buffers” that automatically transfer money from your emergency fund if you’re about to overdraft. It’s like insurance for your checking account.

And inflation? It’s made emergency funds more important than ever. Between 2021 and 2023, the average three-month emergency fund jumped from $9,500 to $11,200 for median-income households. That’s not a suggestion - it’s a reality.

If you’re still using 2020 numbers to plan, you’re already behind.

Final Thought: It’s Not About Money. It’s About Peace.

Carl Richards, a certified financial planner, called emergency funds the “seatbelts of personal finance.” You don’t wear them because you expect to crash. You wear them because you know life doesn’t always go as planned.

When you have a real emergency fund, you sleep better. You say no less. You panic less. You don’t call your parents for money. You don’t lie to your partner about bills. You don’t dread the mail.

You don’t need to be rich to have one. You just need to start. Today. $50. $100. $200. Doesn’t matter. What matters is that you begin - and you keep going.

How much should my emergency fund be?

Aim for three to six months of essential living expenses - rent, utilities, groceries, insurance, transportation, and minimum debt payments. Start with $1,000 if you’re just beginning, then build up. If your income is unstable (freelancer, gig worker), aim for six to nine months.

Where should I keep my emergency fund?

Use a high-yield savings account (HYSA) from banks like Ally, Marcus, or Discover. These offer 4%+ APY, are FDIC-insured, and let you access funds within 1-2 days. Never keep it in checking, stocks, or crypto. It needs to be safe, liquid, and separate.

Can I use my emergency fund for anything unexpected?

Only for true emergencies: unforeseen, essential, and urgent. Examples: car repairs, medical bills, job loss. Not for vacations, new phones, or holiday gifts. Use the two-out-of-three rule - if two of those three traits apply, it qualifies.

What if I use my emergency fund and it’s empty?

That’s okay. Emergency funds are meant to be used. The goal isn’t to never touch them - it’s to avoid debt when life hits. Rebuild it slowly. Set a monthly goal like $100-$200 until you’re back to your target. It’s not failure - it’s working as designed.

Should I build my emergency fund before paying off debt?

If you have high-interest debt (over 7% APR), pay the minimum while saving your first $1,000. Then focus on building your full emergency fund. Once that’s in place, attack the debt aggressively. This balances safety and progress. SoFi and NerdWallet both recommend this approach.

Is a high-yield savings account safe?

Yes. High-yield savings accounts are FDIC-insured up to $250,000 per bank. That means your money is protected even if the bank fails. The interest rate changes, but your principal is safe. Avoid anything labeled as “investment savings” - those are not insured.

How long does it take to build an emergency fund?

Most people build their first $1,000 in 3-6 months by saving $50-$100 per month. Reaching a full three-month fund ($3,000-$6,000) can take 12-24 months, depending on income and expenses. Automation and round-up apps can cut that time by 30-40%.

Do I need an emergency fund if I have good credit?

Yes. Credit cards can help with small emergencies, but they come with risk: interest rates, late fees, and credit score damage if you can’t pay. An emergency fund gives you control - no lender, no terms, no surprises. It’s the only truly reliable safety net.

RAHUL KUSHWAHA

Just started my $1k fund last month with $25/paycheck automation. Got my first tire replacement last week - used $300 and felt zero guilt. 🙌